Click the picture to download a PDF of this story.

By Jesse Carleton, jcarleton@nrha.org, and Liz Lichtenberger, llichtenberger@nrha.org

Lower your costs and increase your revenue. Just about every retailer would agree that’s a great formula for success. But how do you make it happen?

There’s no single, one-size-fits-all solution. Sometimes you need to make major changes; other times the path to greater profitability is paved with a series of micro adjustments to your business.

The first clue to finding the answers might just lie in your financial statements. If you’re watching your numbers closely, you can usually tell when something is amiss. You can also use tools such as the North American Retail Hardware Association’s (NRHA) annual Cost of Doing Business Study, which allows you to compare your financial information with others in the home improvement industry. Doing this comparison can give you another clue that you may be missing opportunities for growth.

If you find areas for improvement, rest assured that you’re likely not the first. Hardware Retailing spoke with five retailers who have found places where their businesses could be driving more profits. Four of those retailers will share their stories on the following pages, and you can find the fifth online at TheRedT.com/tarzian.

Each of these retailers will share suggestions for how to make long-term changes to the way you do business. Each story will focus on different areas, including inventory value, pricing, salesfloor efficiency, labor costs and gross margin. We’ll also identify some of the specific financial performance numbers that will help you review that particular topic. If you need a refresher on how to read the valuable information contained in your financial statements, turn to Page 16 to learn about a new online training course from NRHA.

Inflated Inventory Value

The Challenge

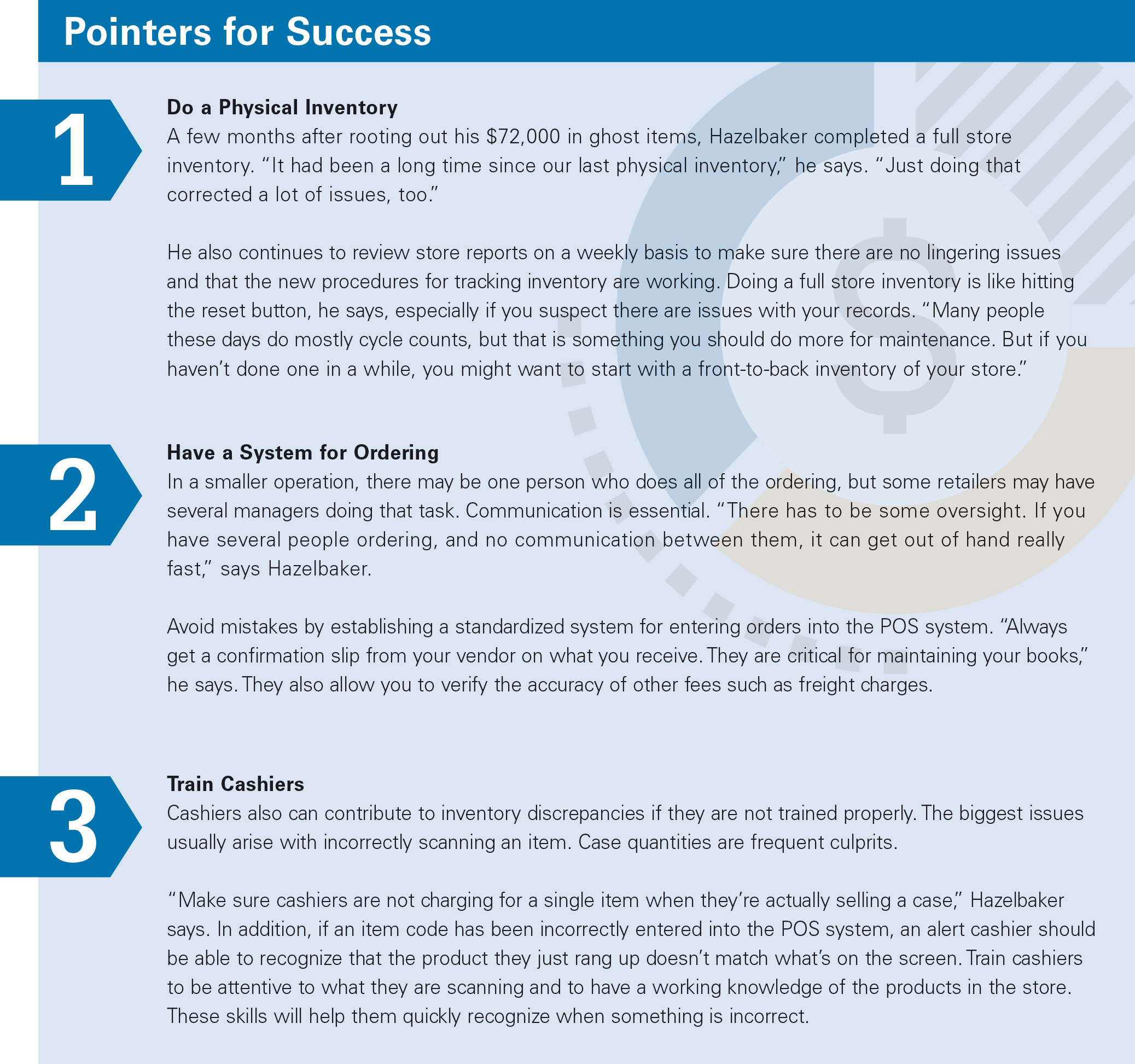

George Hazelbaker had only been working as a manager at the Burns Do it Center in Clovis, New Mexico, for a few years before he started seeing the ghosts.

George Hazelbaker had only been working as a manager at the Burns Do it Center in Clovis, New Mexico, for a few years before he started seeing the ghosts.

“I started noticing a lot of discrepancies in the inventory, or what I call ‘ghost items,’” says Hazelbaker. “There were items that were not correctly accounted for in the POS system.”

Items were appearing on the store’s inventory records that were not actually on the shelves. Most of them had appeared during the company’s recent acquisition of another hardware store in town.

Burns Do it Center includes three locations in New Mexico, in Clovis, Raton and Tucumcari, and one in Texline, Texas. In 2012, just before Hazelbaker took a job with the company, the owners acquired an existing hardware store in Clovis. The change was major. The Clovis Burns Do it Center, formerly a 10,000-square-foot store, relocated to the 20,000-square-foot sales space that previously housed the newly acquired business.

The owners also purchased the store’s existing inventory. To complicate matters, inventory records were stored on a POS system that was different than the one Burns Do it Center used.

“That’s when the problems arose, when we started merging the inventory,” says Hazelbaker. “A lot of the inventory in the store we purchased wasn’t properly accounted for.” Integrating the numbers from two different POS systems meant the details associated with each item, such as the unit of measure, needed to match up with the new system. Much of the time, that integration process worked—other times, it didn’t.

By the time the dust had cleared and the merger was complete, the value of the inventory at Burns Do it Center increased by 250 percent. The increase might seem expected, given that the business had doubled its footprint. Total inventory numbers were still in line with overall industry averages.

But not everything was as it seemed. Hazelbaker began noticing discrepancies, often in the units of measure the POS used to record an item. “For example, some of the wire we sell by the foot, but some of that wire was in our system as if we were selling it by the spool,” he says. “So according to our records, we had 250 spools of wire in our store!”

It’s important to have an accurate record of what’s in the store, but for Hazelbaker, overvaluing the inventory held another more significant threat. A large increase in inventory meant a larger tax bill. “When you have an increase in the valuation of your business, the government sees that as income.” The store’s tax bill was thousands of dollars more than it should have been.

The Solution

It was time to rid the store of its ghost inventory. In addition to the challenges with merging POS records, the company also lacked a standard for purchasing and receiving, which also contributed to the inventory issues, says Hazelbaker. Rather than start by conducting a full inventory of the store, Hazelbaker decided to look first for those problems he could resolve quickly.

“We started by running reports from the POS system for any items with excessive costs,” he says. “We looked for anything that seemed out of the ordinary. If you see $2,000 worth of wire nuts on the report, for example, you know something is wrong. We were looking for that low-hanging fruit that would be easy to spot and take care of.”

He also generated reports that showed all items without a location code in the store, items not sold in the past year and items not counted in over a year. Those particular reports were useful, as Hazelbaker says he found they offered the fastest way to indicate something was off. If, for example, an item hadn’t sold in a year, he should check to see if it was actually on the shelf.

After identifying suspicious items in the report, Hazelbaker or another store manager walked the salesfloor to physically confirm whether those items were indeed in stock.

The results came quickly. Within a few weeks, Hazelbaker had identified $72,000 in ghost inventory. Considering the estimated 34 percent tax on inventory, that was the equivalent of a $20,000 savings, just by keeping more accurate inventory records. By correcting his inventory, he raised his gross margin return on inventory (GMROI) from 132 percent to 148 percent.

Regular Pricing Review

The Challenge

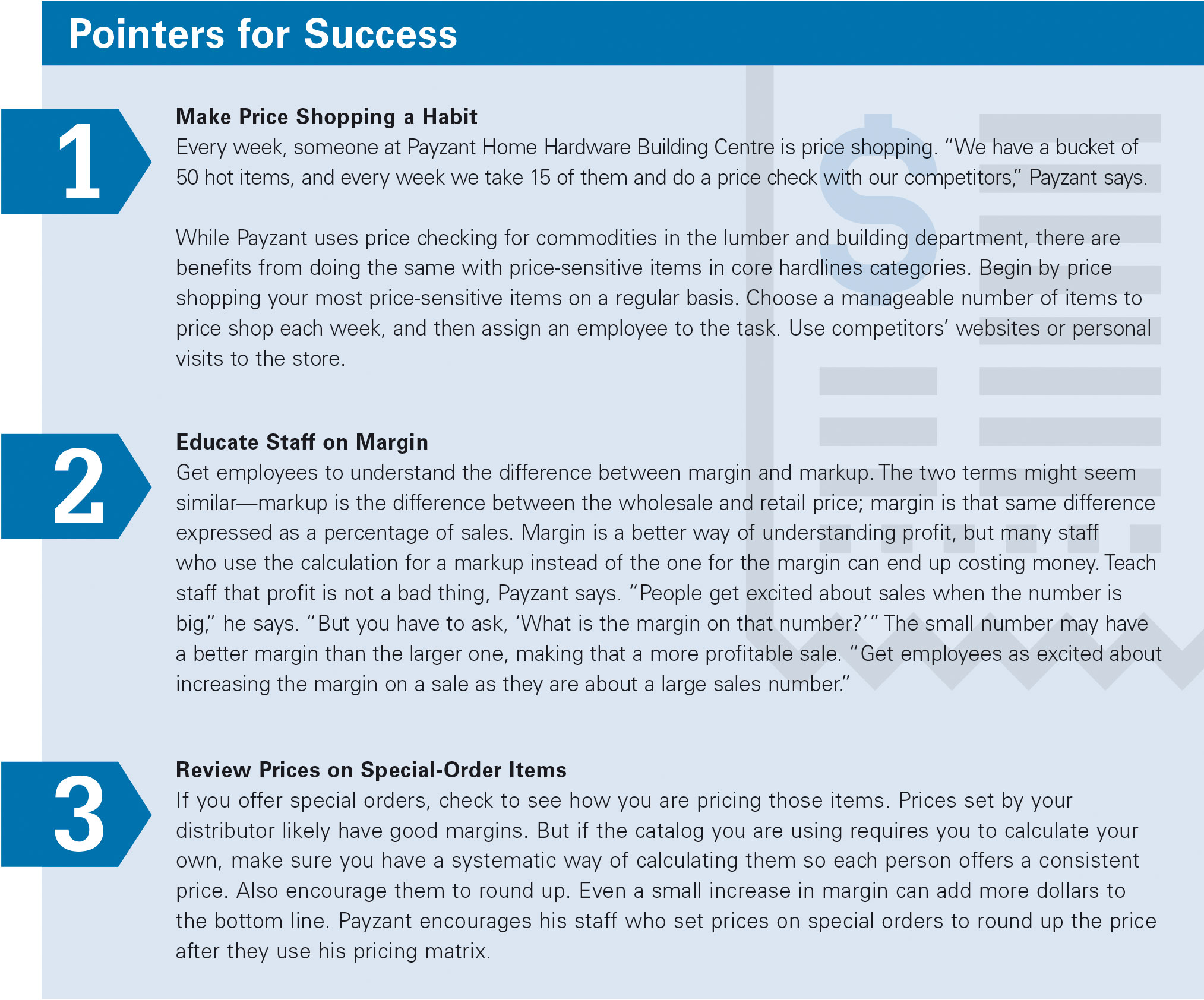

If you don’t regularly review your retail prices, you are likely missing margin opportunities. That’s what Matthew Payzant realized when he started looking at special orders and noncommodity building materials.

If you don’t regularly review your retail prices, you are likely missing margin opportunities. That’s what Matthew Payzant realized when he started looking at special orders and noncommodity building materials.

Payzant is general manager of the family business, Payzant Home Hardware Building Centre, with five locations in Nova Scotia, Canada. The business carries core hardware, along with a full breadth of lumber and building materials. For many items, his wholesaler helps him by updating the recommended retail prices so he maintains a healthy margin above the wholesale cost.

But there is another group of items he buys either directly from the manufacturer or through various building material suppliers. Members of Payzant’s purchasing team are responsible for setting the pricing on those items, and that’s where opportunities can arise. When manufacturers increase their prices, it’s easy to miss out on increasing retail prices in response. The cost-of-goods increases are often gradual and occasional, so sometimes they don’t get noticed, but they erode retailers’ overall margin. “There are items where the prices have continued to creep up,

but we hadn’t always taken the time to check the retails and adjust accordingly,” he says.

Payzant’s special-order process presented similar opportunities. There was not enough consistency in pricing special-order items. “If you went into one of our stores to place a special order and asked five different sales employees the price of a custom door, you might get five different answers,” he says. Besides confusing customers,

it also meant the business was losing margin.

A few missing margin points here and there eventually add up to a lot of missed profits. Payzant needed a way to keep a closer watch on prices, especially in a larger operation where multiple staff members are handling special-order transactions every day. While Payzant runs a lumber business, his strategy for dealing with pricing is applicable to retailers of any size and product mix. A disciplined approach to pricing means you will be making the most of the profit opportunities available

to your business.

The Solution

Payzant needed to address noncommodity building material items and special orders.

Noncommodity building material items are less price-sensitive than commodity items and can provide more margin opportunity. In this category, there were some slow-moving items where retail pricing hadn’t changed in a long time, even if his cost had gone up.

To keep his retails at the appropriate level on these noncommodity items, Payzant instituted a systematic approach to reviewing prices twice a year. He creates a list of all of the items he wants to review and breaks them down into inventory classes. Then he creates a schedule where he can tackle one category per week during the slower times of the year. With help from his staff, he uses price history reports from his POS system to review current prices and margins on each item with those of the past.

“We look at how long it’s been since the last retail price change. Some of the prices we found hadn’t been updated for a couple of years,” he says. If the cost has risen but the retail hasn’t, Payzant can make that adjustment. Checking prices twice a year is generally frequent enough to catch any changes that may have occurred. Of course, commodity items are regularly checked using weekly competitive price checks by telephone and online sources.

“Doing these price checks has enabled us to better protect our margins. There are items where you are making a 35 percent margin, and maybe that looks good,” he says, “but if you used to make a 45 percent margin on that same item, you are losing.”

The second part of Payzant’s pricing challenge revolved around special orders. Staff in the sales department are responsible for giving estimates on special-order items, and sometimes would have a different approach for calculating the price. “People often get comfortable just using a standard multiplier to come up with a selling price and apply the same multiplier to all categories all the time,” he says.

The solution was to create a standardized approach everyone would use. First, Payzant created a price matrix that included all the special-order categories, taking into account margins and appropriate discounts. If a customer is buying vinyl siding, for example, the employee creating the price quote could use the specific multiplier for that item. Payzant also gave his employees extra training on the importance of margin and the impact it has on overall profitability. It may be too early to measure the impact of this standardized pricing strategy on his overall sales numbers, but Payzant is confident that a more systematic approach to margin management in even a small portion of his store will boost overall profits.

Trim Labor Costs

The Challenge

One of the tools Lee Rector at Thomas Home Center True Value in McKinleyville, California, uses to keep a close watch on the overall financial health of his business is NRHA’s Cost of Doing Business Study (CODB). By comparing the numbers on his financial statements to the averages for the industry, he’s found several areas where he could improve his business. A few years ago, labor costs were at the top of the list.

One of the tools Lee Rector at Thomas Home Center True Value in McKinleyville, California, uses to keep a close watch on the overall financial health of his business is NRHA’s Cost of Doing Business Study (CODB). By comparing the numbers on his financial statements to the averages for the industry, he’s found several areas where he could improve his business. A few years ago, labor costs were at the top of the list.

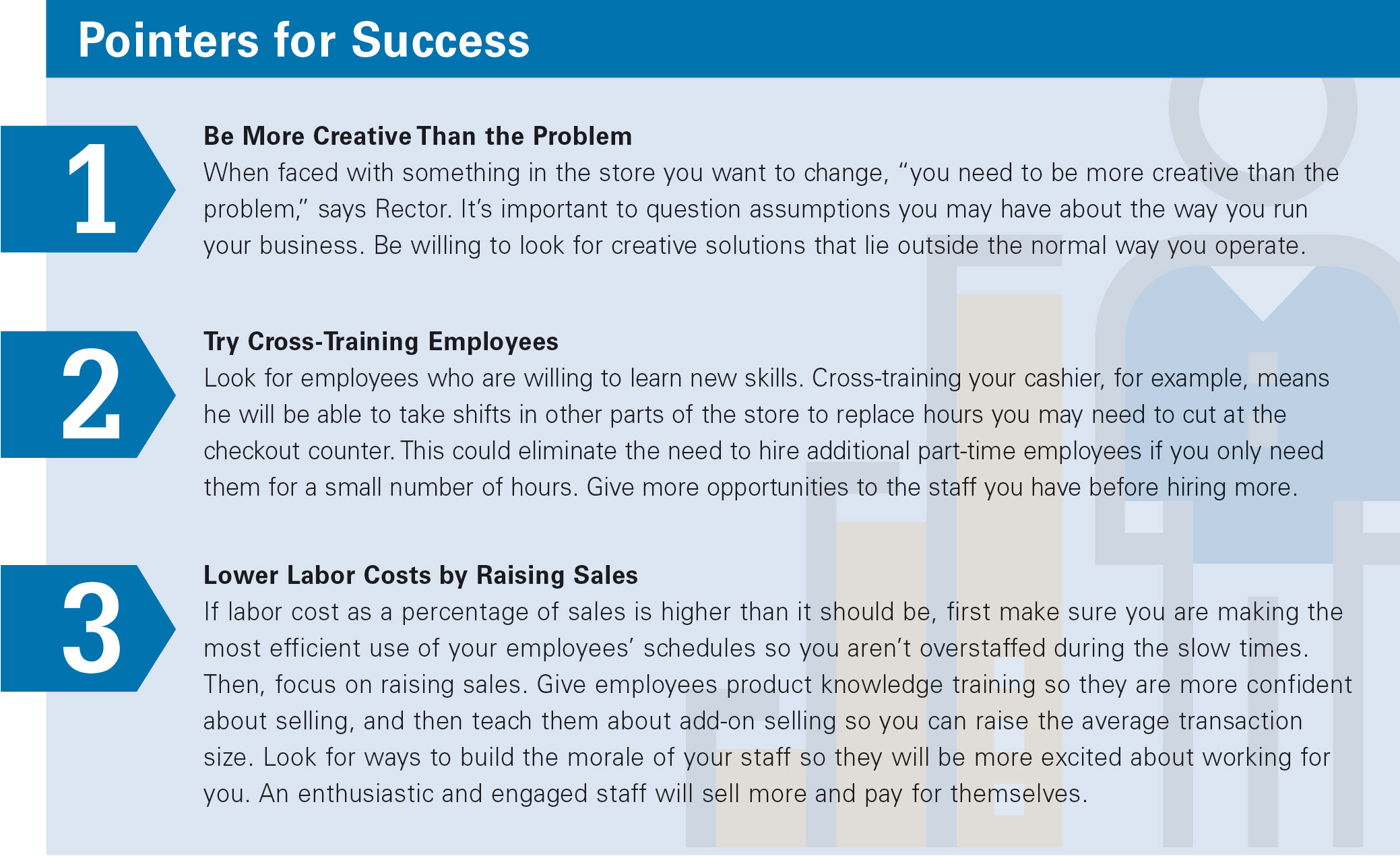

There were a couple of warning signs. His cost of labor as a percentage of sales was a few points higher than the industry average. In addition, as he took a closer look at what was happening on the salesfloor, Rector observed staffing levels were high during points in the day when customer traffic was low.

But lowering labor costs is fraught with challenges. It’s tempting to assume that when you cut labor, your customer service levels will drop and you’ll have to cut employees. Rector did neither, and it turned out to be a win-win for both his business and his employees.

The Solution

To bring down labor costs, Rector says it was obvious he had to lower staffing levels. But what he needed to eliminate first was his preconceived notions about staffing in his store.

To bring down labor costs, Rector says it was obvious he had to lower staffing levels. But what he needed to eliminate first was his preconceived notions about staffing in his store.

“As retailers, we tend to box ourselves into the mindset that we need X number of people for our store to run, even if that means our percentage of labor to sales number is higher than it should be,” he says. “What I found was that most of the time that number can be trimmed. Sometimes it is difficult to achieve, but the labor percentage on NRHA’s CODB is realistic.”

As he tackled a problem, Rector says it was imperative that customer service and sales didn’t suffer. He began cutting back staffing hours during the slower times of the day. At the same time, he made sure his schedule allowed him to help on the salesfloor if necessary. At the end of every week, he took a look at his sales and payroll numbers to see if he was getting closer to his goal, or if he still needed to make adjustments.

“I spent a lot of time listening and watching on the salesfloor, looking where it might make sense to trim staff hours, looking at the sales numbers I wanted to hit and deciding how much I would allow myself to spend on labor,” he says.

Fortunately, trimming labor meant rearranging schedules, not reducing staff. Rector didn’t have to lay off any employees to reduce his labor costs. Instead, he discovered that there were some employees who wanted to work a few less hours. Sometimes it was a college student who was happy to cut back or an older employee who was already hoping they could work one fewer day a week. Rather than make a general announcement that he was going to be cutting hours, Rector had conversations with individual employees and was able to create schedules that worked better than before for each employee while reducing the total amount of money he was spending on payroll.

He also focused on cross-training employees and expanding their skillsets. Besides giving him more flexibility when it comes to scheduling workers, Rector says cross-training also improves customer service and opens up the possibility of some employees even earning more money when they’re able to work a different position in the store.

“I haven’t had to lay anyone off as I’ve been reducing payroll costs,” he says. “I’ve been able to look after my numbers and also take care of my employees. It’s a win-win for everyone.”

Improve Gross Margin

The Challenge

One look at NRHA’s Cost of Doing Business Study last year told Adam Barden he had work to do.

One look at NRHA’s Cost of Doing Business Study last year told Adam Barden he had work to do.

“We knew from looking at that study that our gross margins were below where they really should be for our type of store,” says Barden, who owns Vassar True Value Hardware, with two locations in Vassar and Frankenmuth, Michigan. “At that point, we set some very specific goals about where we wanted those numbers to be and then talked about the different ways we could get there.”

His two stores have quite a bit in common. Both are in rural markets, with each home to about 3,000 people. Both markets include independent stores as competitors, and both are about 30 minutes from the big boxes. Both also see a customer mix of about 70 percent DIYers and 30 percent contractor and industrial business. In both stores, lawn and garden is the top-selling department, and paint is second.

Even with the commonalities, Barden had his work cut out for him. He quickly determined that a thorough review of pricing in both stores would provide the biggest impact and the fastest way to see some movement in gross margin numbers.

The Solution

The first thing Barden did was reach out to his co-op to ask for assistance. The co-op helped complete a pricing study of the marketplace, and from there, Barden and his team came up with a pricing profile. He spent most of February updating pricing across the board at both locations. It was a big task, but February was an ideal time to do it since business was a little slower.

“We did the pricing study for both of our stores,” Barden says, “Then we went through and made pricing changes throughout each location.” Now, the team regularly updates and improves the pricing throughout the store.

“We may have some areas where we can be more competitive and others where we’re giving away too much margin. We’re continuing to find opportunities for improvement.”

Barden focused heavily on pricing in his top-selling department, lawn and garden. “There are a lot of lower-margin items, like yard goods—mulches and soils and things like that—where, if you can make a small change, you can see quite a difference in your margins,” he says.

When building a pricing profile, Barden chose to look at prices under two different lenses. “We found some of the suggested retail pricing from our co-op was too aggressive—it would make our margins too low,” he says. “But one level of variable pricing was too high, especially on highly visible and high-dollar items. So we came up with a customized system between the two.”

He says they now try to be more competitive on items above $25 or items that are highly visible, including anything customers might frequently price shop. For items below $25 or those that aren’t highly visible and are less likely to be price shopped, the prices might be a little higher.

Another step for Barden and his team was to look at the commodity items they sell, such as water softener, birdseed and dog food. “We had to make some decisions to either raise prices or discontinue certain items and bring in others in their place,” he says.

Barden saw small results right away, and about six months later, he was seeing more differences month to month. “We’re two or three margin points up over last year, which tells me we’re moving the needle in the right direction,” he says.